#Digital Printing

Industrial printer shipments increased more than 17% year over year in 2021, according to IDC

"Shipments were slower in the second half of the year than the first half in most regions," said Tim Greene, research director, Hardcopy Solutions at IDC. "We're hearing about supply chain and inventory challenges from many of the global suppliers. Despite this, printer shipment numbers for the year were much stronger than 2020. And, with the exception of North America, the global market is still not back to pre-pandemic shipment levels."

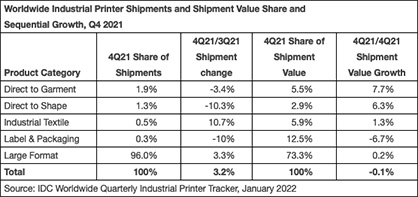

Worldwide Industrial Segment Highlights for Q4 2021

• Large format digital printer shipments grew 3.2% worldwide in 4Q21 compared to 3Q21.

• Dedicated direct-to-garment (DTG) printer shipments declined 3.5% sequentially in 4Q21. IDC believes this is partially due to the impact of aqueous direct-to-film printers.

• Direct-to-shape printer shipments grew 10% quarter over quarter in 4Q21.

• Digital label & packaging printer shipments declined 11% sequentially in 4Q21.

• Industrial textile printer shipments grew more than 10% in 4Q21, continuing a strong performance for the full year 2021.

Regional Analysis

• The strongest growth came from the Central Europe, Middle East & Africa (CEMA) region which saw shipments grow more than 26% quarter over quarter in 4Q21.

• Total shipments in the Asia/Pacific region (including China) were essentially flat for 4Q21.

• Japan and North America both declined in 4Q21 when compared to 3Q21.

• Shipments in the Western European market grew nearly 14% quarter over quarter in 4Q21.

• The Europe, Middle East, and Africa (EMEA) region declined 12.5% compared to Q3 2021.

Outlook for 2022

• The year 2021 was considerably better than 2020 as a whole and there are still important segments of the market such as the trade show business that has not fully resumed. IDC expects stronger shipment numbers driven by great demand in those segments in 2022.

• Mix changes drove a separation between shipment trend and revenue trend through the course of the 2021, with more low-end units sold which subtracted revenue from the worldwide industrial printer hardware market.

IDC's Worldwide Quarterly Industrial Printer Tracker provides total market size and vendor share for five major market categories: large format, label and packaging, direct to garment, industrial textile, and direct to shape. In addition to units, shipment value, and ASP, the Tracker also provides market results for each product category by ink type, media size, hardware class, or primary application across nine geographic regions and 90 countries.